Case Study - Student Loan Strategy as a Resident

Why is Your Student Loan Plan Crucial as a Resident or Fellow?

Let's explore a case study featuring Jane Doe, a Resident Physician with $250,000 in federal student loans at a 7% interest rate.

Meet Jane Doe:

Current Salary (Residency): $80,000

Residency Duration: 3 years

Future Attending Salary: $350,000

Employer Offers: 4% Match on 403(b) contributions

Loan Repayment Plan: Enrolled in the IBR plan and eligible for Public Service Loan Forgiveness (PSLF)

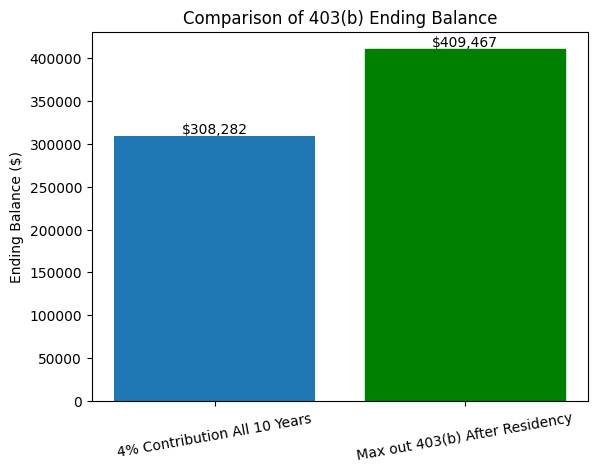

Scenario 1: Consistent 4% 403(b) Contribution Over 10 Years

Jane contributes 4% to her 401(k) throughout the entire 10-year period.

With an 8% annualized return, that balance would grow to $308,282.

Scenario 2: Max Out 403(b) Contributions After Residency

Jane contributes 4% to her 403(b) during residency.

After residency, she maxes out her 403(b) contributions with $24,500 annually.

With an 8% annualized return, that balance would grow to $409,467.

Student Loan Repayment Strategies:

During Residency:

Jane enrolls in the PAYE/IBR plan, setting her monthly payment at $441.

As an Attending Physician:

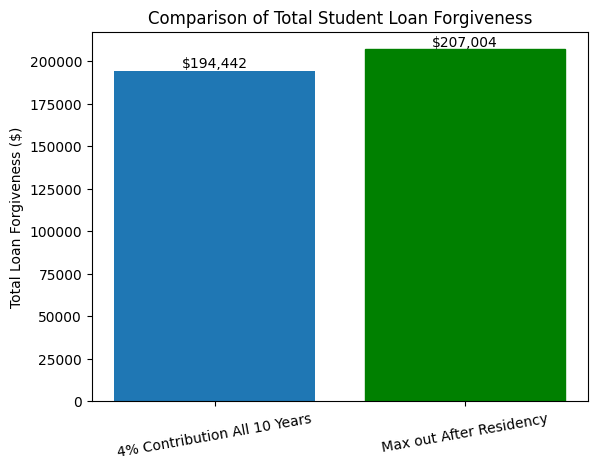

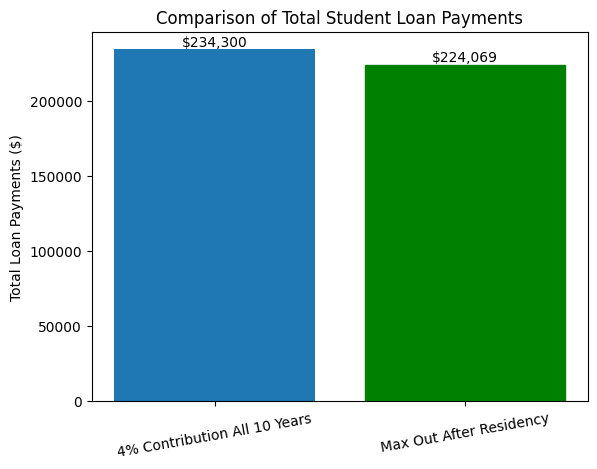

If Jane continues saving only 4% to her 403(b), her monthly student loan payment would increase to $2,601. After 120 qualifying payments towards PSLF, she would be eligible for $194,442 in forgiveness. In total, she would have paid $234,300 in loan payments.

If Jane maxes out her 401(k) contributions with $24,500 annually, her monthly payment decreases to $2,498. After 120 qualifying payments towards PSLF, she would be eligible for $207,004 in forgiveness. In total, she would have paid $224,069 in loan payments.

Savings from Maxing Out Her 401(k):

Jane would save $10,231 in total student loan payments.

She would increase her tax-free forgiveness amount by $12,562

Additionally, she would accumulate $101,185 more towards retirement by maxing out her 403(b) once she starts her Attending role.

Why is This Important?

Residency or fellowship is the perfect time to start planning your financial future. With lower income during these years, strategic planning can significantly reduce the total amount you pay before qualifying for forgiveness under PSLF.

Key Takeaway: Strategic planning during residency paves the way for a more secure financial future. The choices you make now can have a lasting impact on your student loan repayment and retirement goals.

Schedule a free consultation if you want to learn how strategies like this could fit into your plan.